The long-standing debate between renting and buying a home often dismisses “rent money” as “dead money”—an expense yielding no return. However, a strict “buy-at-all-costs” approach can overlook significant avenues for wealth creation as well as financial flexibility for individuals and businesses alike. While generations have been taught that homeownership is the sole path to prosperity, the financial reality of renting is far more intricate, offering distinct advantages that, when leveraged effectively, can lead to substantial wealth growth combined with adaptability.

The common saying, “Every dollar spent on rent could instead be contributing to a mortgage, building equity, and securing a future asset,” isn’t always the optimal path. This is precisely where Investmate enters as a game-changer. With our deep understanding together with strategic financial planning, guided by expert insights, we help clients make financially astute choices. This unlocks pathways to wealth creation, emotional security, perceived stability, and the potential for capital appreciation—rather than rent being merely a financial outflow.

Australia’s Rental Market: A Snapshot of Rising Costs and Burden

To grasp the present scenario, it’s crucial to examine the trends in the Australian rental market and their repercussions on households. Recent data highlights the increasing pressure on renters:

Rental Inflation vs. CPI Rent Index:

- Advertised rents surged 5% over the year to March 2025, reaching a record median of $630/week nationally.

Source: australianpropertymarket.com.au

- The CPI-derived rent index showed a 4.8% annual increase in December 2024, down from 8.1% in 2023 but still above overall inflation.

Source: theguardian.com.

Rent Burden on Households:

- As of January 2025, it is projected that middle-income Australians spend approximately 33% of their wages on rent—the highest in CoreLogic records since 2006.

- Since Covid, rents have risen a staggering 36.1%, an extra ~$171 weekly ($8,884 annually).

Source: theguardian.com.

- Low Vacancy Rates: Vacancy rates fell to ~1%, half the historical norm (~2.5%)—driving upward rent pressure.

- Unit Rents Surging: In early 2025, unit rents grew faster than houses—units +8–10% YoY in Brisbane and Adelaide too, in contrast to houses at +5–6%.

Source: australianpropertymarket.com.au.

The Nuances of Renting: More Than Just an Expense

While rent payments don’t directly enhance equity, they provide significant and often underappreciated advantages that can be strategically utilized for financial gain. Not all rent money is “dead” in the traditional sense.

- Flexibility and Mobility: Renting offers immense flexibility to relocate for career opportunities and lifestyle changes, together with evolving family needs. You avoid the significant transaction costs (stamp duty, agent fees, legal costs) and time associated with buying as well as selling property. This mobility can translate into higher earning potential in conjunction with greater life satisfaction in a fast-paced economy.

- Lower Upfront Costs: The barrier to entry for renting is substantially lower than for buying. Beyond a bond and initial rent, there are no stamp duties, large deposits, or immediate legal and inspection fees. This frees up capital that can be invested elsewhere, potentially generating returns that outpace property appreciation, especially for those disciplined with their savings.

- Reduced Maintenance and Holding Costs: Homeowners bear the full burden of property maintenance, repairs, council rates, water rates, strata fees, and building insurance—expenses that can be significant as well as uncertain in a way. Renters are typically exempt from these expenses, allowing for a clearer, more predictable budget. The money saved can be directed towards investments coupled with other financial goals.

- Market Hedging and Risk Mitigation: Renting can serve as a form of market hedging. In property market downturns, renters are insulated from negative equity and falling asset values. They can strategically wait for market corrections or more favorable buying conditions without being tied down by a depreciating asset—a powerful tool for risk-averse investors as well as those timing their market entry.

- Lifestyle and Experiential Value: Beyond financial considerations, renting can offer a superior lifestyle, allowing individuals to live in desirable areas they might not afford to buy in. This reduces commuting times and provides access to better amenities in conjunction with enhancing overall quality of life. The psychological freedom from property-related stress also holds considerable value.

The True Cost of Homeownership: Beyond the Mortgage Repayments

The financial burden of homeownership extends far beyond the principal as well as interest repayments. Overlooking these additional costs can lead to severe financial strain along with negating the perceived benefits of property acquisition.

Upfront Costs:

- Stamp Duty: A significant state government tax, often tens of thousands of dollars, paid upfront.

- Lender’s Mortgage Insurance (LMI): If your deposits fall short of 20% of the property’s value, this insurance safeguards the lender rather than you, adding thousands to your loan.

- Legal Fees and Conveyancing: Costs associated with the transfer of ownership.

- Building and Pest Inspections: Essential checks before purchase.

- Loan Establishment Fees: Fees charged by the lender.

Ongoing Costs:

- Interest Payments: Especially in the early years, a considerable amount of repayments is directed towards interest, which doesn’t enhance equity. With current interest rates, this component can be substantial.

- Council Rates: Annual or quarterly payments to the local council.

- Water Rates: Service and usage charges too.

- Insurance: Building insurance is mandatory; however, contents insurance is also highly recommended.

- Maintenance and Repairs: From routine upkeep to unexpected emergencies, these costs can be unpredictable and substantial.

- Strata Fees/Body Corporate Fees: For apartments/townhouses, these regular fees cover the maintenance of common areas and building insurance, combined with administrative costs.

When these myriad costs are factored in, the total out-of-pocket expense for homeowners can often significantly exceed rental payments, especially in the short to medium term.

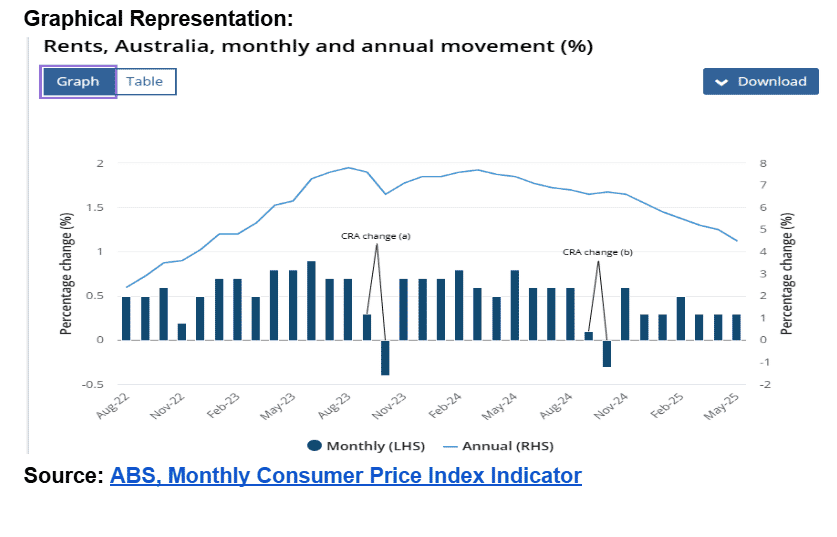

Monthly Rental Price Changes in Australia (January – June 2025)

| Month | Monthly Rental Price Change (%) | Annual Rental Price Change (%) |

| January | +0.3% | +5.8% |

| February | +0.2% | +5.5% |

| March | +0.3% | +5.2% |

| April | +0.4% | +5.0% |

| May | +0.3% | +4.5% |

Source: ABS, Monthly Consumer Price Index Indicator

The Strategic Advantages of Renting

For many, renting offers undeniable strategic advantages, particularly in a volatile economic climate:

- Flexibility and Mobility: Renting provides unparalleled flexibility, allowing easy relocation for job opportunities, lifestyle changes, or evolving circumstances without the significant transaction costs together with market risks of selling a property. This agility is a considerable asset in a fast-paced economy.

- Lower Upfront Costs: The upfront cost of renting is considerably less than that for buying, freeing up substantial funds that can be invested elsewhere. This capital can be a potent catalyst for wealth creation in a way if utilized strategically.

- Reduced Financial Responsibilities: Renters are generally free from property maintenance burdens together with repairs and unexpected ownership costs. This translates into less stress and more predictable monthly expenses, allowing for better financial planning as well as budgeting.

- Diversified Investment Opportunities: The most compelling argument against “rent money is dead money” lies in the power of diversified investment. Capital not tied up in property can be invested in a well-diversified portfolio of stocks, bonds, managed funds, or a personal business. Over time, these alternative investments could potentially generate returns that outpace property appreciation in a way, especially when factoring in the ongoing costs of homeownership.

Making an Informed Decision

Ultimately, the choice between renting and buying should not be based on outdated maxims or societal pressure but on a comprehensive analysis of one’s individual circumstances together with prevailing market conditions. It demands a forward-looking perspective, weighing the tangible and intangible costs and benefits of each option. Consider:

- Your Financial Health: What is the status of your income stability, savings rate, and any debts you currently have?

- Your Investment Horizon: How long do you plan to stay in one location?

- Your Lifestyle Needs: Do you value flexibility over permanence?

- Market Conditions: Is it a buyer’s, seller’s, or balanced market in your desired location? What are the projections for interest rates and property values?

- Opportunity Cost: What could you do with the money saved by not buying immediately?

End Thoughts: Making the Right Choice

The assertion that “rent money is dead money” oversimplifies a complex decision-making process. Renting can offer financial flexibility, lifestyle adaptability, and opportunities for diversified investments. As the housing market continues to evolve, it is crucial to assess individual circumstances and long-term goals too.

At Investmate, we are committed to empowering clients with the knowledge together with resources necessary to navigate these decisions confidently. Our expertise ensures that whether you choose to rent or buy, your choice aligns with your aspirations and financial well-being.

Call now at 61421942049 or book your free consultation call and learn how to use rent purposefully—not just as an expense, but as part of a winning wealth strategy.