What Buyers Should Expect from Australia’s Housing Market in 2026

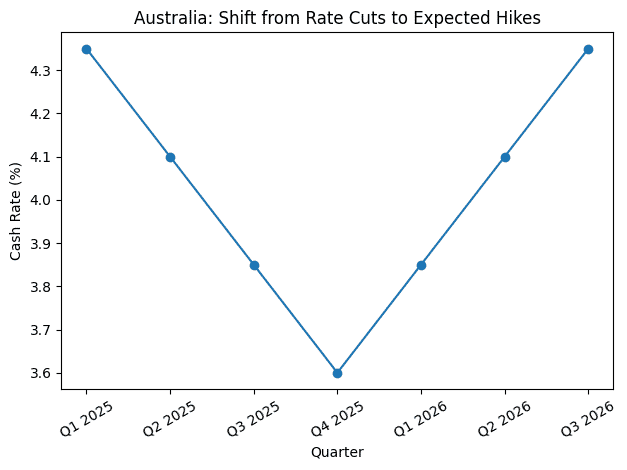

Australia’s housing market is entering 2026 with stronger-than-expected momentum. The RBA’s recent report notes markets now price in around two cash rate rises this year, reflecting hotter inflation and jobs data. At the same time, the cuts last year have already eased borrowing costs and sparked a pick-up in lending. Banks have rolled through rate cuts to home loans, and credit growth is up around its long-term average. In practice, this means demand has stayed surprisingly firm.

Employment is high, and many buyers, from first-home and downsizing owner-occupiers to investors, remain active. Overall, the market is shifting gears but not reversing course. Strong underlying demand (backed by low unemployment and healthy household balance sheets) is still there even as higher rates cool some buyers.

Strong Credit and Investor Activity

Competition among lenders and supportive credit conditions are giving many buyers room to move. The RBA notes that total credit growth has picked up and is above its long-run average. Housing loan approvals have risen solidly, driven in particular by investors. In fact, investor loan commitments are growing at their fastest pace in years. The share of new loans going to landlords has climbed over recent months, keeping upward pressure on prices. For buyers, this means they often compete with cashed-up investors bidding for the same properties. We’re seeing investors chase yield in many markets, especially where rents are rising and stock is limited, which keeps competition high.

Standalone Houses vs Apartments

Traditionally, Australian buyers have favoured detached houses over units for land value and growth. Many clients still see houses as a safer, longer-term play. However, in some cities, high-quality apartments have attracted strong demand on affordability and rental yield grounds. (For example, recent market analysis shows a rising share of apartment markets matching house growth.) On balance, though, the supply of new units remains constrained in some areas, and standards are improving. As buyers’ agents, we note that good standalone homes on land are still very popular – they often enjoy broader buyer appeal and more stable price performance, especially in family-friendly suburbs. Apartments can outperform in tight inner-city pockets, but they tend to be chosen by downsizers, investors and first-timers looking for entry-level prices.

Affordable Suburbs and Supply Pockets

Affordability pressures have steered buyers toward lower-priced homes. In 2025, more affordable quartiles saw stronger growth (about +1.1%) than the upper price bracket (+0.2%). This “flight to affordability” means middle-ring and outer suburbs – especially those with good schools, transport links or job access – have led the market. Regional centres and growth corridors are also booming: for instance, regional Western Australia saw house values jump ~16% in 2025 and parts of regional Queensland ~12% as buyers spread out.

At the same time, supply shortages are a key theme. Both new construction and resale listings are tight across much of the country, putting a floor under prices. We’re seeing that in many suburbs, even modest demand keeps prices stable. In effect, low inventory means prices aren’t falling sharply – they’re just growing more slowly. In premium markets (inner Sydney/Melbourne), demand has softened first, giving savvy buyers more room to negotiate. Here, sellers are more open to offers, especially on high-end homes, as buyers hesitate under higher mortgage costs.

Investor Competition & Negotiation Power

Investors are increasingly shaping buyer strategies. With rents rising (vacancies ~1.3%) and population growth strong, investors are still active. This means owner-occupier buyers often face extra bids on good properties. A well-prepared buyer – with finance pre-approval and cash flow buffers – can still find opportunities. As one strategist notes, prepared buyers can use any weaker sentiment as a chance to negotiate. In other words, where momentum cools (especially in pricey markets), buyers with secure funding may have more bargaining power.

Overall, higher rates mean most markets will grow more slowly, but we’re not expecting a crash. Supply constraints and sustained demand mean prices should hold up in 2026. Standalone houses in affordable, supply-constrained areas tend to be most resilient. Premium segments may plateau sooner, giving room to negotiate for astute buyers. We advise clients to focus on fundamentals, location, yield, and long-term drivers, rather than short-term forecasts. As always, a sound strategy and preparation are key to success.

Ready to make your move? For tailored advice or to discuss your buying strategy, contact Investmate. If you’re serious about your next purchase, call us at +61 421 942 049 or book a free consultation today. At Investmate, we’re here to guide you through this market and help secure the right property.

Follow Investmate on Instagram and LinkedIn for more insights on Australia’s property market.