The Australian property market has long been a beacon of resilience, a strong narrative woven into the national identity. Are interest rates and inflationary pressures finally about to curtail the Australian property market? This question is at the forefront of every investor’s mind. For years, the market has greatly demonstrated remarkable resilience, defying expectations and pushing property values to new heights. As 2025 unfolds, the confluence of high interest rates and persistent inflationary pressures presents a complex and evolving landscape in some way. On the contrary, the recent period of high inflation, basically followed by the RBA’s aggressive monetary policy tightening, introduced a new level of uncertainty.

At Investmate, we have been seamlessly monitoring this new epoch evolution, greatly helping you understand the nuances of this market and position yourself for long-term success. We truly believe that with the right strategy, together with a profound understanding of market trends, these economic headwinds are not a roadblock but a catalyst for informed, strategic decision-making.

The Interplay between Interest Rates and Inflation

The relationship between interest rates and inflation is central to understanding the current market climate. A high inflation environment, strictly driven by factors like global supply chain issues and domestic demand, forces central banks like the RBA to raise interest rates. The primary goal is to cool down the economy by making borrowing more expensive, which in theory reduces spending and brings inflation back into a target range in a unique manner.

For the Australian property market, this has a direct and immediate impact. Higher interest rates increase mortgage repayments, reducing borrowing capacity and squeezing household budgets, which often results in a moderation in property price growth, as prospective buyers become more cautious and less competitive. The principal concern for many has been whether this combination of a higher cost of living (inflation) and higher cost of borrowing (interest rates) would trigger a sharp as well as sustained price correction.

The Shifting Dynamics of Interest Rates and Inflation

Inflationary pressures quietly remained a key concern for the first half of 2025. The June quarter CPI meticulous data showed inflation settling at a level that, while lower than its peak, remained above the Reserve Bank of Australia’s (RBA) target range. This greatly led to continued vigilance from the RBA, which held the cash rate steady for much of the period.

The effect of high interest rates has been a dual one.

- On affordability: Higher borrowing costs have undoubtedly tested the serviceability of mortgages, particularly for first-home buyers as well as those with high loan-to-value ratios. This has cooled the frenetic pace of some segments of the market.

- On investor behavior: It has also created a more discerning environment. Adept investors are no longer simply riding a wave of capital growth but are now meticulously focused on yield, location, and the fundamentals of a property.

While the easing of inflation and interest rates has been a positive development, it has basically created a fascinating dynamic in the property market. On one hand, reduced borrowing costs have enhanced buyer capacity & sentiment. On the other, the enduring repercussions of the previous high-interest-rate landscape and cost-of-living pressures have kept affordability under strain in some manner.

Beyond the Headlines: The True Drivers of Market Momentum

So, why has the market not succumbed to these pressures? Several major factors are at play:

- Supply Constraints: A persistent housing shortage, particularly in major capital cities, simply continues to act as a floor for prices. Despite government initiatives, construction has been unable to keep pace with demand from a growing population, which greatly includes both natural growth and significant migration.

- Strong Labor Market: The Australian labor market remained remarkably robust through the first half of the year, with low unemployment rates. This basically provides a sense of financial security that underpins housing demand and a borrower’s ability to service their loan.

- Renewed Investor Confidence: Following a period of uncertainty, investors have returned to the market, capitalizing on the relative stability and long-term capital growth potential of property.

- Changing Demographics: A continued shift in living preferences, with more single-person households and a desire for more living space, is creating new pockets of demand that cannot be met by the current housing stock.

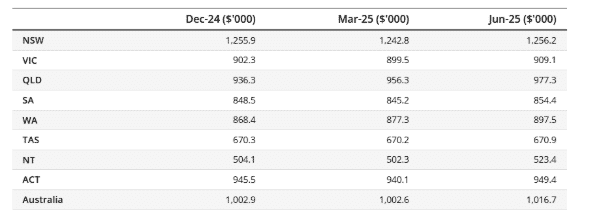

Statistical Insights: What the Data Says About the Australian Property Market

Source: Australian Bureau of Statistics

This table shows that while there was a slight dip in the March quarter of 2025, the overall trend from December 2024 to June 2025 was one of continued growth. The mean dwelling cost for Australia as a whole has risen, with notable increases in Western Australia and Queensland, illustrating the differing performances across regions.

The Investmate Advantage: Your Partner in a Changing Market

The property market’s relationship with inflation and interest rates is a cyclical one, but understanding where we are in that particular cycle is the key to success. According to the data, the Australian property market is not on the brink of collapse; rather, it is undergoing a fundamental shift towards a more balanced and strategic environment. Instead, it is recalibrating in response to current economic conditions. For those looking to enter or expand their property portfolio, this period presents a unique opportunity in some manner.

In a market defined by complexity, having an expert on your side is not a luxury—it’s a necessity.Call now at +61-421-942-049 or book your free consultation call with Investmates’ dedicated and seasoned professionals to take your first step towards a smarter property investment journey.